Everything You Need To Know About House Mortgages

Content author-Donovan AlexandersenAre you a mortgage loan veteran? The mortgage marketing is constantly undergoing changes, for people buying their first homes to the people seeking to refinance. You need to keep up on these changes in order to get the best mortgage for your situation. Read on to learn more about home mortgages.

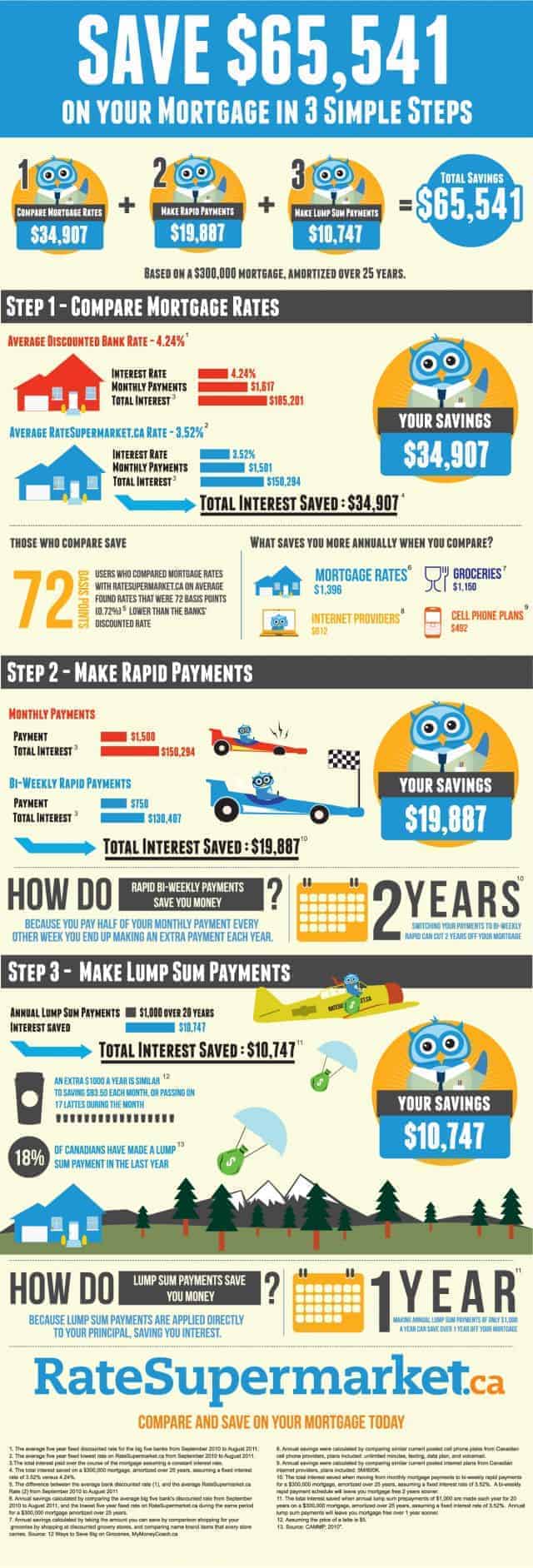

If a 20% down payment is out of your league, do some shopping around. Different banks will have different offers for you to consider. Terms and rates will vary at each, some will give a lower downpayment, but a slightly higher interest rate. Look for the best mix for your current situation.

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

If you can afford a higher monthly payment on the house you want to buy, consider getting a shorter mortgage. Most mortgage loans are based on a 30-year term. A mortgage loan for 15 or 20 years may increase your monthly payment but you will save money in the long run.

Be sure to compare the different term options that are available for home mortgages. You could choose between a number of options, including 10, 15 and 30 year options. The key is to determine what the final cost of your home will be after each term would be up, and from there whether or not you would be able to afford the mortgage each month for the most affordable option.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Find out if the loan you are applying for is a fixed rate or adjustable rate loan. Generally adjustable rate loans offer lower interest rates; however, the interest rate can increase over time. With an adjustable rate loan, your interest rate can increase yearly; thus costing you more money in the long run.

Monitor interest rates before signing with a mortgage lender. If the interest rates have been dropping recently, it may be worth holding off with the mortgage loan for a few months to see if you get a better rate. Yes, it's a gamble, but it has the potential to save a lot of money over the life of the loan.

A good credit score is essential if you want to finance a home. If your score is below 600 you have some work to do before you can hope to purchase a home. Begin by getting a copy of your credit record and verifying that all the information on it is correct.

Do not embark on the process of buying a home if you have just started a new job within the last year. The best home mortgage rates go to those that have been with a company for a number of years. Having mouse click the up coming web site for a short time is seen as a risk, and you will be the one to pay for it with a higher interest rate.

Pay your credit cards on time if you are considering a home mortgage in the next few years. Your credit score and debt to income ratios will come into play when you go for a home mortgage. If you have multiple late payments or are carrying a lot of debt, you may find the mortgage offers you receive to be poor.

One type of loan that is not normally talked about is an interest only loan. This type of loan allows you to make low monthly payments for a certain period, then the payment amount increases. These loans are generally used to help you get into a home at a low monthly payment.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

If you have a lot of open credit cards, consider paying them off and closing the accounts before applying for a home loan. Many lenders look negatively upon the overuse of credit. So, by closing your credit card accounts, you can show that you are a worthy credit risk for the lender.

Be careful about quicksand mortgages. These are mortgages that have all sorts of hidden tricks in them like balloon payments, prepayment penalties, tons of upfront fees, and more. These loans typically are only helpful to the lender, not to the customer. In fact, they can make your loan down right unaffordable over time.

Never sign home mortgage paperwork that has blank spaces. Also, make sure you initial each page after you read it. This ensures that terms cannot be added after you sign. Unscrupulous lenders may be inclined to add pages to your contract which you did not read, and this protects you from this practice.

Try not to take a mortgage for the entire amount you can afford. If you take the absolute maximum, you won't have much money left as a cushion when your payments come due. If anything unexpected comes up, you may end up in a real pickle if you are spending the most every month.

Remember that most lenders only guarantee an interest rate for a maximum of six months before you take the mortgage. That means you can apply for a mortgage before actually finding a house to buy, or before you can move your mortgage to a different lender, but don't take too long!

All in all, you will be satisfied with your mortgage if you use what you have now learned. You never want to feel like you've made a decision that will cost you years of your life's finances. Getting the mortgage you deserve helps keep everything in order and helps provide for your family.